Inside Angle

From 3M Health Information Systems

Moving the spotlight toward the Gulf

Countries across the Gulf region are experiencing a vibrant period of health systems financing “transform-mania.” Current rigid health systems cannot meet rising population demands, nor accommodate ever-rising provider requests for more funding, so health system reconfiguration and transformation is an inevitable process. In fact, in many of these changes are already underway, with some countries moving quickly while others explore their options. Across the region, flights are packed with hundreds of consultants who are continuously inventing and reinventing different types of reforms. Luckily today, and contrary to last century’s “black box” reforms[1], we are well equipped to deliver “sonar fish-finding expedition” type of reforms. These types of reforms can be carefully designed using international best practices and knowledge. Most importantly, health policy makers have the opportunity to choose from a plethora of tools and methodologies to make these reforms successful.

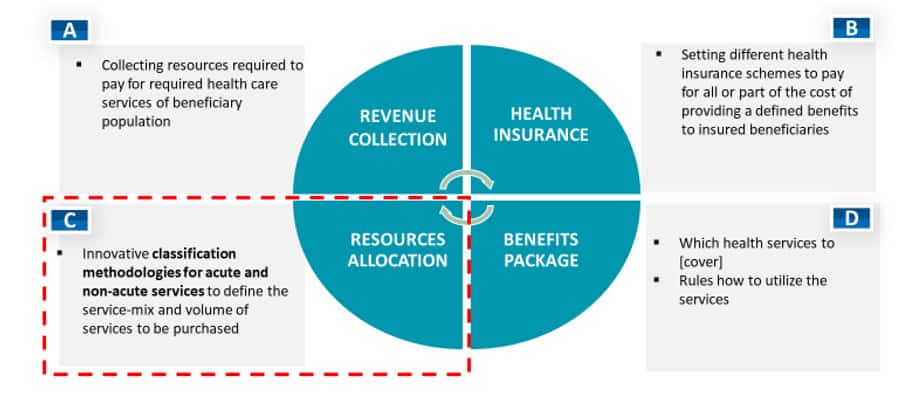

Health systems across the Gulf are in different states of maturity, but all are in the process of performing various types of health system reimbursement reform. By focusing on key health system financing functions[2] (Figure 1), we can identify high level priority needs:

These predominantly oil-driven economies are not suffering from a lack of funding (See Component A), but they are still required to explore alternative funding options and introduce various cost-sharing strategies with beneficiaries. Private health insurance is rather well developed across the region, but public health insurance is lagging behind (Component B, e.g. KSA, Kuwait).

The Kingdom of Saudi Arabia is on its way to introducing a public health insurance scheme. A new health insurance agency called Program for Health Allocation and Purchasing (PHAP) is being set up. Under this new agency, health systems will be reorganized into clusters (20-25, each covering approximately 1 million people). The clusters will be funded by allocated capitation from the central level. A mandatory requirement for the new public insurance system is to improve current provider data collection and data management capacities. This is expected to improve public hospitals’ health management capacities in order to better forecast future patient demands and resources allocation needs.

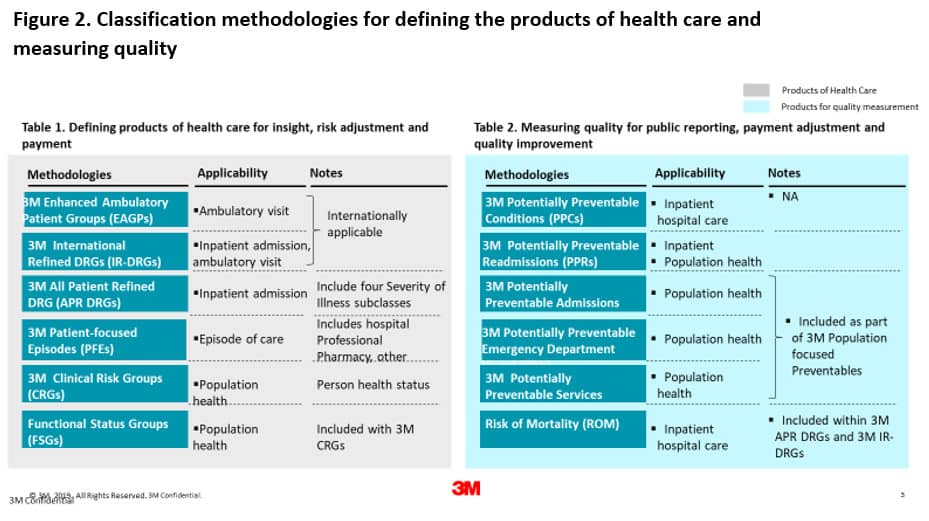

Kuwait is also reforming quickly, as the country is facing a dramatic increase in patient demands. Today, public providers are paid for using block budgets based on historical data. This means of organization gives no visibility to the type of services delivered to patients, and there are no incentives to improve. On the other hand, private hospitals are paid via a fee for service method that is draining the health budget and must be changed very soon. Here the priorities are to introduce minimal data set requirements and standards as well as to implement appropriate classification methodologies for paying inpatient and ambulatory services (3M is contributing a comprehensive array of approaches that may be of interest for some countries Figure 2).

The Emirate of Dubai has moved to introduce mandatory DRG reporting for inpatient services. Starting in 2020, Dubai Health Authority will introduce the new IR-DRG classification[3]. All providers will be equipped with new software solutions designed to improve coding accuracy as well as to improve health system information management capacities, among other things.

Undoubtedly, the most advanced and bold reforms are unfolding in the Emirate of Abu Dhabi. Abu Dhabi is the front runner in introducing innovative solutions across the region. The new and forthcoming changes are expected to entirely revamp health system reimbursement for both inpatient and ambulatory services. On the inpatient side, updated IR-DRG classification will replace the IR-DRG 2012 version. The most exciting aspect of the forthcoming reforms is in the ambulatory sector. Faced with the constant pressure to increase the budget for health care, the health leadership of the Emirate realized the need to assign a limit to the escalating costs. The new reforms will address widespread concerns about unnecessary overutilization of high cost (and medically unjustified) ambulatory services (read ancillary services). The current fee for service method of payment for ambulatory services will be replaced with an advanced state of the art ambulatory patient grouping system. The new ambulatory classification system is carefully designed to address specific local needs. Its implementation will cut growing cost escalation and is expected to influence the behavior of payers and providers who will now be incentivized to steer patients towards higher quality and efficiency. These upcoming changes are bold but seen as necessary from both the regulator and payer perspective. Providers are also aware that they must increase efficiency in the way they run their services. The successful implementation of planned reforms will reward high-quality performing providers and will put pressure on the “free riders.” If implemented as planned, by the end of 2020 the first pilot project should be rolled out to assess the impact of these reforms over the entire healthcare ecosystem.

The pace of health system reimbursement reforms across the Middle East does not stop here. Almost all countries need to design new or refine their current benefit packages (Component D, e.g, KSA, UAE, Kuwait, Oman, Bahrain, Qatar)[4].

In discussing health system financing reforms, the time has come to move the spotlight from the USA and Western Europe towards the Gulf. Fantastic innovations are in the pipeline and many countries can learn from these developments.

Vladimir Lazarevik is lead 3M health economist across Middle East.

References

[1] New insurance billing system in Dubai hospitals from 2020, Gulf news, available at: https://gulfnews.com/uae/health/new-insurance-billing-system-in-dubai-hospitals-from-2020-1.66043223

[2] Defining Benefits Package: More tips for emerging markets (Available at: https://www.mckinsey.com/industries/healthcare-systems-and-services/our-insights/defining-a-health-benefits-package)

[3] McIntyre D, Borghi J. Inside the black box: modeling health care financing reform in data-poor context. Available at: https://academic.oup.com/heapol/article/27/suppl_1/i77/602246

[4] Schieber G et al. Financing Health Systems in the 21st Century. Available at: https://www.ncbi.nlm.nih.gov/books/NBK11772/

Vladimir Lazarevik, MD, MPH

Health Economist

Vladimir Lazarevik, MD, MPH, is lead 3M health economist across Middle East. Vladimir has deep health care content knowledge and premium consulting experience in managing multiple projects of varying complexity.…